The Turf War To Issue Currency

February 9, 2018 Leave a comment

To be able to issue currency or determine what passes for money and on what terms, is the ability to impose your will on others and settle deals in your favour.So small wonder that governments, bankers, billionaires and would-be-billionaires see the benefit in fighting to issue money. Go back to history and you see kings have issued currency, bankers/ moneychangers/ money movers and central bankers have issued currencies and then again desperate societies have often come up with tokens for use amongst themselves…………The same old game is playing out again.

Following speech is a sample of a banker trying to ally with state power to squish private money issuers. Read the arguments,file them away for future reference. If you hear these arguments repeated in the media, know them for the propaganda they are. Are they all rubbish arguments? NO. But neither are they the whole story. And passively swallowing them doesn’t serve your best interests.

Money in the digital age: what role for central banks?

Lecture by Agustín Carstens

General Manager, Bank for International Settlements

House of Finance, Goethe University

Frankfurt, 6 February 2018Introduction

Good morning, ladies and gentlemen. Thank you for that kind introduction, Jens. I am very happy to be here at this prestigious university and to be part of this impressive lecture series sponsored by Sustainable Architecture for Finance in Europe (SAFE), the Center for Financial Studies (CFS) and the Deutsche Bundesbank. I would also like to thank Professor Brigitte Haar for being such a generous host today. It is an honour to discuss money at an event organised by the Bundesbank, which has been a beacon of stability since its foundation some 60 years ago.

As Jens can attest, being a central banker is a fascinating job. In fact, it is a privilege. During the last decade it has been anything but quiet in the central banking world. We have been confronted with extraordinary circumstances that have required extraordinary policy responses. In such an environment, it has been of the utmost importance to share experiences and lessons learnt among central banks, creating a body of knowledge that will be there for the future.

One of the reasons that central bank Governors from all over the world gather in Basel every two months is precisely to discuss issues at the front and centre of the policy debate. Following the Great Financial Crisis, many hours have been spent discussing the design and implications of, for example, unconventional monetary policies such as quantitative easing and negative interest rates.

Lately, we have seen a bit of a shift, to issues at the very heart of central banking. This shift is driven by developments at the cutting edge of technology. While it has been bubbling under the surface for years, the meteoric rise of bitcoin and other cryptocurrencies has led us to revisit some fundamental questions that touch on the origin and raison d’être for central banks:

• What is money?

• What constitutes good money, and where do cryptocurrencies fit in?

• And, finally, what role should central banks play?The thrust of my lecture will be that, at the end of the day, money is an indispensable social convention backed by an accountable institution within the State that enjoys public trust. Many things have served as money, but experience suggests that something widely accepted, reliably provided and stable in its command over goods and services works best. Experience has also shown that to be credible, money requires institutional backup, which is best provided by a central bank. While central banks’ actions and services will evolve with technological developments, the rise of cryptocurrencies only highlights the important role central banks have played, and continue to play, as stewards of public trust. Private digital tokens posing as currencies, such as bitcoin and other crypto-assets that have mushroomed of late, must not endanger this trust in the fundamental value and nature of money.

What is money?

“What is money?” is obviously a key question for any central banker, and one on which economists have spent much ink. The answer depends on how deep and philosophical one wants to be. Being at a university, especial y one named after Goethe, I think I can err on the side of being philosophical. Conventional wisdom tells you that “money is what money does”. That is, money is a unit of account, a means of payment and a store of value. But telling you what something does, does not really tell you what it is. And it certainly does not tell you why we need or have money, how it comes about and what the preconditions are for it to exist.

In terms of the “need” for money, you may learn that money is a way to get around the general lack of double coincidence of wants. That is, it is rare that I have what you want and you have what I want at the same time. As barter is definitely not an efficient way of organising an economy, money is demanded as a tool to facilitate exchange.

What about the other side of the coin, so to speak? How does money come about? Again, conventional wisdom may tell you that central banks provide money, ie cash (coins and notes), and commercial banks supply deposits. But this answer is often not fully satisfactory, as it does not tell why and how banks should be the one to “create” money.If you venture into more substantive analyses on monetary economics, things get more complex. One theory, which proposes that “money is memory”, amounts to arguing that a “superledger” can facilitate exchange just like money. This argument says a ledger is a way of keeping track of not only who has what but also who owes, and is owed, what. I will come back to this later. Moving beyond this line of thought, other scholarly and historical analyses provide answers that

are more philosophical. These often amount to “money is a convention” – one party accepts it as payment in the expectation that others will also do so. Money is an IOU, but a special one because everyone in the economy trusts that it will be accepted by others in exchange for goods and services. One might say money is a “we all owe you”.Many things have served as money in that way: Yap stones, gold coins, cigarettes in war times, $100,000 bills, wissel (Wechsel), ie bills of exchange or bearer notes, such as those issued by the Bank of Amsterdam in the first half of the 17th century. It includes an example from my own country, Aztec hoe (or axe) money, a form of (unstamped) money made of copper used in central Mexico and parts of Central America.

Common to most of these examples is that the nominal value of the items that have served at one time as money is unrelated to their intrinsic value. Indeed, as we know very well in the case of fiat money, the intrinsic value of most of its representations is zero.

History shows that money as a convention needs to have a basis of trust, supported by some form of institutional arrangement. As Curzio Giannini puts it: “The evolution of monetary institutions appears to be above all the fruit of a continuous dialogue between economic and political spheres, with each taking turns to create monetary innovations … and to safeguard the common interest against abuse stemming from partisan interests.”

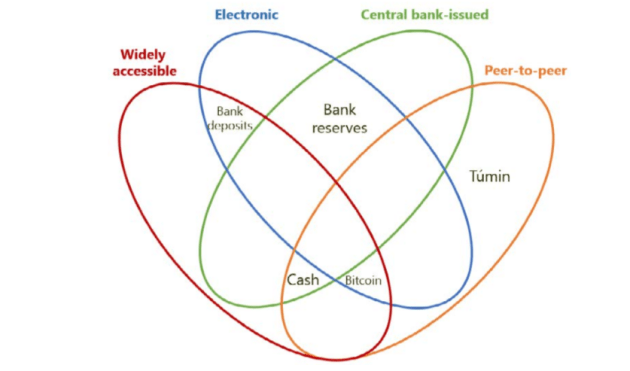

Money can come in different institutional forms and colours. How to organise them? The paper by Bech and Garratt in last September’s BIS Quarterly Review presented the money flower as a way of organising monies in today’s environment. It acknowledges that money can take on rather different forms and be supplied in various ways.

The money flower :

Allow me to explain, noting that we do not sell seeds to this money flower!

The money flower highlights four key properties on the supply side of money: the issuer, the form, the degree of accessibility and the transfer mechanism.• The issuer can be either the central bank or “other”. “Other” includes nobody, that is, a particular type of money that is not the liability of anyone.

• In terms of the form it takes, money is either electronic or physical.

• Accessibility refers to how widely the type of money is available. It can either be wide or limited.

• Transfer mechanism can either be a central intermediary or peer-to-peer, meaning transactions occur directly between the payer and the payee without the need for a central intermediary.Let us look at where some common types of money fit into the flower, starting with cash (or bank notes) as we know it today. Cash is issued by the central bank, is not electronic, is available to everyone and is peer-to-peer. I do not need a trusted third party such as Jens to help me pay each of you 10 euros.

Let us try another one: bank deposits. They are not the liability of the central bank, mostly electronic, and in most countries available to most people, but clearly not peer-to-peer. Transferring resources from a bank deposit requires the involvement of at least your own bank, perhaps the central bank and the recipient’s bank. Think here not only of commercial bank deposits but also bills, eg non-interest bearing (bearer) certificates, issued privately, as in the case of the Bank of Amsterdam mentioned earlier.

Local or regional currencies are the ones that can be spent in a particular geographical location at participating organisations. They tend to be physical. The túmin, for example, was a local currency circulating (illegally) for some time around 2010 exclusively in the Mexican municipality of Espinal.

What does digitalisation mean for the flower? Digitalisation is nothing new: financial services and most forms of money have been largely digital for many years. Much of the ongoing transformation is just adding a mobile version for many services, which means that the device becomes a virtual extension of the institution. As such, there is not a new model. The money flower then also easily accommodates these forms.

That is also the case for the digital, account-based forms of money that central banks traditionally have made available to commercial banks and, in some instances, to certain other financial or public institutions (ie bank reserves).

It would also be the case if the central bank were to issue digital money to the wider public for general purposes. Each central bank will have to make its own decision on whether issuing digital money is desirable, after considering factors such as the structure of the financial system and underlying preferences for privacy. The central bank community is actively analysing this issue.A potentially important and leapfrogging digital-related development, however, is distributed ledger technology (DLT), the basis for Bitcoin. Many think DLT could transform financial service provision,

maybe first wholesale, then possibly retail. For example, it could enhance settlement efficiency involving securities and derivatives transactions. A few central banks have conducted experiments in this area, for example the Bank of Canada, the Bundesbank, the Monetary Authority of Singapore and the Bank of England. Yet doubts remain regarding the maturity of DLT and the size of associated efficiency gains relative to existing technologies. Moreover, their robustness, including to cyber-risk, is still to be fully understood and ascertained. Still, there are potential benefits, and I expect that central banks will remain engaged on this topic.For now, DLT is largely used to “create” bitcoin and other digital currencies. Such cryptocurrencies can be placed easily in the money flower. Nobody issues them, they are not physical and they are peer-to-peer. But beyond that, how should one think about them?

What constitutes good money?

Just because we are able to find a place for bitcoin in our money flower does not mean we should consider it as “good” money. As I mentioned before, trust is the fundamental tenet that underpins credible currencies, and this trust has to be earned and supported. There are many lessons from history and institutional economics on the earning of trust that we can use as we move further into digitalisation.

Over the ages, many forms of private money have come and gone. It is fair to say that the same has happened with various experiments with public money (that is, money issued by a public entity that is not the central bank). While some lasted longer than others, most have invariably given way to some form of central bank money. The main reason for their disappearance is that the “incentives to cheat” are simply too high. Let me give three historical examples: one in Germany, another in the United States and the last one in Mexico.

In Germany, the Thirty Years War (1618–48), involving small German states of the Holy Roman Empire and neighbouring regional powers, was associated with one of the most severe economic crises ever recorded, with rampant hyperinflation – just as happened three centuries later during the Weimar Republic – and the breakdown of trade and economic activity. The crisis became known as the Kipper- und Wipperzeit (the clipping and culling times), after the practice of clipping coins (shaving metal from their circumference) and sorting good coins from bad. This morning, we are launching a BIS Working Paper, by Professor Isabel Schnabel and BIS Economic Adviser Hyun Song Shin, which further details and explains this experience, as background to my speech.

While episodes of currency debasement have occurred throughout history, this one stands out for two reasons. First is the severity of the crisis and its rapid regional spread. Debasement proceeded at such a pace that public authorities quickly lost control of the downward spiral. Second is how the debasement was brought under control. This occurred through standardisation of wholesale payments by public deposit banks, for example the Bank of Hamburg and the Bank of Amsterdam. These were in many ways examples of the precursors of modern central banks. As the working paper argues, monetary order could be brought to an otherwise chaotic situation by providing reliable payment means through precursors to central bank money, which at the end means the use of a credible institutional arrangement.

In the period in the United States known as the Free Banking Era, from 1837 to 1863, many banks sprang up that issued currency with no oversight of any kind by the federal government. 10 These so-called free bank notes did not work very well as a medium of exchange. Given that there were so many banks of varying reputations issuing notes, they sold at different prices in different places, making transactions quite complicated. And as supervision was largely absent, banks had limited restraint in issuing notes and did not back them up sufficiently with specie (gold or silver), thereby debasing their values. This era of “wildcat banking” ended up being a long and costly period of banking instability in the history of the US, with banking panics and major disruptions to economic activity. It was, after some further hiccups, followed by the establishment of the Federal Reserve System in 1913.

Let me present a final example, from Mexican monetary history. A little known fact is that Mexico had the first series of hyperinflations at the beginning of the 20th century. My country had a revolution from 1910 to 1921, in which no central government existed in an effective way, with many factions fighting and disputing different territories. A winning faction would arrive in a territory, print its own money and make void previously issued cash. So different bills issued by different factions coexisted, leading to chaos and hyperinflation. To give you an idea of the disorder, in 2015 four trunks full of bills were returned to Mexico after having been appropriated by the US Navy in 1914, when the US occupied the port city of Veracruz. In the trunks, the Bank of Mexico discovered dozens of types of bills that the central bank had not even known existed. At the end of the conflict, a new constitution was drafted, having as a central article one which gave the Bank of Mexico the appropriate institutional framework, designating it the exclusive issuer of currency in the country. Once this was in place, hyperinflation ceased, illustrating the importance of controlling fiscal dominance (which tends to be the result of the abuse of publicly issued money).

Based on these experiences, most observers, and I suspect all of you here, would agree that laissez-faire is not a good approach in banking or in the issuance of money. Indeed, the paradigm of strict bank regulation and supervision and central banks overseeing the financial and monetary system that has emerged over the last century or so has proven to be the most effective way to avoid the instability and high economic costs associated with the proliferation of private and public monies.

The unhappy experience with private forms of money raises deep questions about whether the proliferation of cryptocurrencies is desirable or sustainable. Even if the supply of one type of cryptocurrency is limited, the mushrooming of so many of them means that the total supply of all forms of cryptocurrency is unlimited. Added to this is the practice of “forking”, where an offshoot of an existing cryptocurrency can be conjured up from thin air. Given the experience with currency debasement that has peppered history, the proliferation of such private monies should give everyone pause for thought. I will return to this shortly.

We have learned over the centuries that money as a social institution requires a solution to the problem of a lack of trust. The central banks that often emerged in the wake of the private and public money col apses may not have looked like the ones we have today, but they all had some institutional backing. The forms of this backing for their issuance of money have differed over time and by country. Commodity money has often been the start. History shows that gold and other precious metals stored in the vault with governance (and physical) safeguards can provide some assurance. Commodity money is not the only or necessarily sufficient mechanism. Often it also required a city-, state- or nation-provided charter, as with the emergence of giro banks in many European countries.

Later, the willingness of central banks to convert money for gold at a fixed price (the gold standard) was the mechanism. Currency boards, where local money is issued one-to-one with changes in foreign currency holdings, can also work to provide credibility.

The tried, trusted and resilient modern way to provide confidence in public money is the independent central bank. This means legal safeguards and agreed goals, ie clear monetary policy objectives, operational, instrument and administrative independence, together with democratic accountability to ensure broad-based political support and legitimacy. While not fully immune from the temptation to cheat, central banks as an institution are hard to beat in terms of safeguarding society’s economic and political interest in a stable currency.

Where do cryptocurrencies fit in?

One could argue that bitcoin and other cryptocurrencies’ attractiveness lies in an intelligent application of DLT. DLT provides a method to broadcast transactions publicly and pseudonymously in a way that achieves in principle ledger immutability.Who would have thought that having people guessing solutions to what was described to me by a techie as the mathematical equivalent of mega-sudokus would be a way to generate consensus among strangers around the world through a proof of work? Does it thus provide a novel solution to the problem of how to generate trust among people who do not know each other? If DLT provides the potential for a superledger, could bitcoin and other cryptocurrencies then substitute for some forms of money? We do not have the full answers, but at this time the answer, also in the light of historical experiences, is probably a sound no, for many reasons. In fact, we are seeing the type of cracks and cheating that brought down other private currencies starting to appear in the House of Bitcoin. As an institution, Bitcoin has some obvious flaws.

Debasement. As I mentioned, we may be seeing the modern-day equivalent of clipping and

culling. In Bitcoin, these take the form of forks, a type of spin-off in which developers clone Bitcoin’s

software, release it with a new name and a new coin, after possibly adding a few new features or tinkering

with the algorithms’ parameters. Often, the objective is to capitalise on the public’s familiarity with Bitcoin

to make some serious money, at least virtually. Last year alone, 19 Bitcoin forks came out, including Bitcoin

Cash, Bitcoin Gold and Bitcoin Diamond. Forks can fork again, and many more could happen. After all , it

just takes a bunch of smart programmers and a catchy name. As in the past, these modern-day clippings

dilute the value of existing ones, to the extent such cryptocurrencies have any economic value at all.Trust. As the saying goes, trust takes years to build, seconds to break and forever to repair. Historical experiences suggest that these “assets” are probably not sustainable as money. Cryptocurrencies are not the liability of any individual or institution, or backed by any authority. Governance weaknesses, such as the concentration of their ownership, could make them even less trustworthy. Indeed, to use them often means resorting to an intermediary (for example, the bitcoin exchanges) to which one has to trust one’s money. More generally, they piggyback on the same institutional infrastructure that serves the overall financial system and on the trust that it provides. This reflects their challenge to establish their own trust in the face of cyber-attacks, loss of customers’ funds, limits on transferring funds and inadequate market integrity.

Inefficiency. Novel technology is not the same as better technology or better economics. That is clearly the case with Bitcoin: while perhaps intended as an alternative payment system with no government involvement, it has become a combination of a bubble, a Ponzi scheme and an environmental disaster. The volatility of bitcoin renders it a poor means of payment and a crazy way to store value. Very few people use it for payments or as a unit of account. In fact, at a major cryptocurrency conference the registration fee could not be paid with bitcoins because it was too costly and slow: only conventional money was accepted. To the extent they are used, bitcoins and their cousins seem more attractive to those who want to make transactions in the black or illegal economy, rather than everyday transactions. In a way, this should not be surprising, since individuals who massively evade taxes or launder money are the ones who

are willing to live with cryptocurrencies’ extreme price volatility. In practice, central bank experiments show that DLT-based systems are very expensive to run and slower and much less efficient to operate than conventional payment and settlement systems. The electricity used in the process of mining bitcoins is staggering, estimated to be equal to the amount Singapore uses every day in electricity, making them socially wasteful and environmentally bad. Therefore, the current fascination with these cryptocurrencies seems to have more to do with a speculative mania than any use as a form of electronic payment, except for illegal activities. Accordingly, authorities are edging closer and closer to clamping down to contain the risks related to cryptocurrencies.There is a strong case for policy intervention. As now noted by many securities markets and regulatory and supervisory agencies, these assets can raise concerns related to consumer and investor protection. Appropriate authorities have a duty to educate and protect investors and consumers, and need to be prepared to act. Moreover, there are concerns related to tax evasion, money laundering and criminal finance. Authorities should welcome innovation. But they have a duty to make sure technological advances are not used to legitimise profits from illegal activities.

What role for the central bank?

Central banks, acting by themselves and/or in coordination with other financial authorities like bank regulators and supervisors, ministries of finance, tax agencies and financial intelligence units, may also need to act, given their roles in providing money services and safeguarding money’s real value. Working with commercial banks, authorities have a part to play in policing the digital frontier. Commercial banks are on the front line since they are the ones settling trades, providing real liquidity, keeping exchanges going and interacting with customers. It is alarming that some banks have advertised “bitcoin ATMs” where you can buy and sell bitcoins. Authorities need to ensure commercial banks do not

facilitate unscrupulous behaviours.Central banks need to safeguard payment systems. To date, Bitcoin is not functional as a means of payment, but it relies on the oxygen provided by the connection to standard means of payments and trading apps that link users to conventional bank accounts. If the only “business case” is use for illicit or illegal transactions, central banks cannot allow such tokens to rely on much of the same institutional infrastructure that serves the overall financial system and freeload on the trust that it provides. Authorities should apply the principle that the Basel Process has adhered to for years: to provide a level playing field to all participants in financial markets (banks and non-banks alike), while at the same time fostering innovative, secure and competitive markets. In this context, this means, among other things,

ensuring that the same high standards that money transfer and payment service providers have to meet are also met by Bitcoin-type exchanges. It also means ensuring that legitimate banking and payment services are only offered to those exchanges and products that meet these high standards. Financial authorities may also have a case to intervene to ensure financial stability. To date, many judge that, given cryptocurrencies’ small size and limited interconnectedness, concerns about them do not rise to a systemic level. But if authorities do not act pre-emptively, cryptocurrencies could become more interconnected with the main financial system and become a threat to financial stability. Most importantly, the meteoric rise of cryptocurrencies should not make us forget the important role central banks play as stewards of public trust. Private digital tokens masquerading as currencies must not subvert this trust. As history has shown, there simply is no substitute.Still, central banks are embracing new technologies as appropriate. Many new developments can help. For example, fintech and “techfin” – which refers to established technology platforms venturing into financial services. These are changing financial service provision in many countries, most clearly in payments, and especial y in some emerging market economies (for example, China and Kenya). While they introduce the possibility of non-bank financial institutions introducing money-type instruments, which raises a familiar set of regulatory questions, they do present scope for many gains.

Conclusion

In conclusion, while cryptocurrencies may pretend to be currencies, they fail the basic textbook definitions. Most would agree that they do not function as a unit of account. Their volatile valuations make them unsafe to rely on as a common means of payment and a stable store of value. They also defy lessons from theory and experiences. Most importantly, given their many fragilities, cryptocurrencies are unlikely to satisfy the requirement of trust to make them sustainable forms of money. While new technologies have the potential to improve our lives, this is not invariably the case. Thus, central banks must be prepared to intervene if needed. After all, cryptocurrencies piggyback on the institutional infrastructure that serves the wider financial system, gaining a semblance of legitimacy from their links to it. This clearly falls under central banks’ area of responsibility. The buck stops here. But the buck also starts here. Credible money will continue to arise from central bank decisions, taken in the light of day and in the public interest. In particular, central banks and financial authorities should pay special attention to two aspects. First, to the ties linking cryptocurrencies to real currencies, to ensure that the relationship is not parasitic. And second, to the level playing field principle. This means “same risk, same regulation”. And no exceptions allowed.