They Can’t Both Be Right

May 30, 2014 2 Comments

Stock markets have been touching new highs over past six months on improved sentiment, but macro concerns have kept bond yields high.Historically, cheap money, or low interest rates, has been a pre-condition for a bull run in equities. Given that interest rates in India are at multi-year highs, the question is who is right -the bond investor or the equity investor?

Stock markets have been touching new highs over past six months on improved sentiment, but macro concerns have kept bond yields high.Historically, cheap money, or low interest rates, has been a pre-condition for a bull run in equities. Given that interest rates in India are at multi-year highs, the question is who is right -the bond investor or the equity investor?

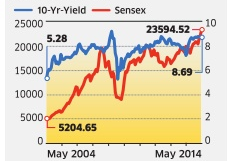

The story of the last six months in these two markets has been different. The benchmark Sensex has rallied over 20%, but the bond yields have continued to remain high above 8.6% in the period, suggesting the equity rally is purely driven by sentiment, and not by economic fundamentals. At the beginning of the 2004-2007 bull run, the 10-year government bond yields were at 5.28%, which increased to 7.8% towards end 2007 (the Sensex rose from 4800 to 20000 during the period). The bond yield fell to 5.26% in December 2008 as the Reserve Bank of India joined global central banks in lowering interest rates to prevent a worldwide collapse of economies after Lehman Brothers went bankrupt. That formed the base for another rally from 2009 to 2011; the Sensex rose from 8600 to 20500 in the period.The benchmark bond yields are now at 8.69%, close to a five-year high. Read more of this post