Stock markets have been touching new highs over past six months on improved sentiment, but macro concerns have kept bond yields high.Historically, cheap money, or low interest rates, has been a pre-condition for a bull run in equities. Given that interest rates in India are at multi-year highs, the question is who is right -the bond investor or the equity investor?

Stock markets have been touching new highs over past six months on improved sentiment, but macro concerns have kept bond yields high.Historically, cheap money, or low interest rates, has been a pre-condition for a bull run in equities. Given that interest rates in India are at multi-year highs, the question is who is right -the bond investor or the equity investor?

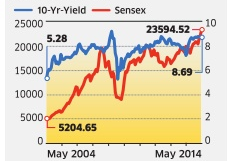

The story of the last six months in these two markets has been different. The benchmark Sensex has rallied over 20%, but the bond yields have continued to remain high above 8.6% in the period, suggesting the equity rally is purely driven by sentiment, and not by economic fundamentals. At the beginning of the 2004-2007 bull run, the 10-year government bond yields were at 5.28%, which increased to 7.8% towards end 2007 (the Sensex rose from 4800 to 20000 during the period). The bond yield fell to 5.26% in December 2008 as the Reserve Bank of India joined global central banks in lowering interest rates to prevent a worldwide collapse of economies after Lehman Brothers went bankrupt. That formed the base for another rally from 2009 to 2011; the Sensex rose from 8600 to 20500 in the period.The benchmark bond yields are now at 8.69%, close to a five-year high. Read more of this post

According to Sunil Jaiwal, CEO of Sumansa Exhibitions, the organisers of the Indian Property Show in Dubai,Mumbai is the top investment destination for UAE-based non-resident Indians (NRIs),Bangalore is second. Chennai and Pune are jointly in the third position with an almost equal percentage of people preferring these cities.Delhi comes at the fourth place, followed by Cochin, Navi Mumbai, Gurgaon and Hyderabad.

According to Sunil Jaiwal, CEO of Sumansa Exhibitions, the organisers of the Indian Property Show in Dubai,Mumbai is the top investment destination for UAE-based non-resident Indians (NRIs),Bangalore is second. Chennai and Pune are jointly in the third position with an almost equal percentage of people preferring these cities.Delhi comes at the fourth place, followed by Cochin, Navi Mumbai, Gurgaon and Hyderabad. 1 Seize Every Opportunity : Look out for opportunities out side your scope of work. Never hassle yourself too much with the motive of defeating your competitor. Rather, invest all energies on a bigger goal to add strength and power to your business.

1 Seize Every Opportunity : Look out for opportunities out side your scope of work. Never hassle yourself too much with the motive of defeating your competitor. Rather, invest all energies on a bigger goal to add strength and power to your business. 2.Win Allies: Five brothers won against a hundred.How do you think the Pandavas did that? The relationships they established over the years paid off. You may be busy focusing on your own growth at the present, but you must start reaching out to more people and making allies. They will push you forward when the time comes.

2.Win Allies: Five brothers won against a hundred.How do you think the Pandavas did that? The relationships they established over the years paid off. You may be busy focusing on your own growth at the present, but you must start reaching out to more people and making allies. They will push you forward when the time comes.  The following is an excerpt from a Rakesh Jhunjhunwala interview in the ET on the 27th of this month. Prescience?Wisdom?Wishful thinking?Motivated sound bytes?……….Time will tell.I thought it best to record the words for easy future reference.Here’s waiting for the structural and secular bull market that RJ speaks about!

The following is an excerpt from a Rakesh Jhunjhunwala interview in the ET on the 27th of this month. Prescience?Wisdom?Wishful thinking?Motivated sound bytes?……….Time will tell.I thought it best to record the words for easy future reference.Here’s waiting for the structural and secular bull market that RJ speaks about!